E3 has published a first-of-a-kind analysis and report that rigorously quantifies the grid and customer impacts of continued data center growth in Virginia, the world’s leading data center market, in the context of that state’s ambitious clean energy targets. As the electric industry transitions to an era of rapid load growth driven largely by the near-term rise in computing demands, the potential impacts of data centers will be profound and transformative. This work was conducted on behalf of the Virginia Joint Legislative Audit and Review Commission (JLARC), and the work informed JLARC’s recommendations to the Virginia legislature on potential policy actions and areas for continued study, which can be found here.

Our report finds that the sustained scale and pace of data center growth in the region will likely be constrained by new energy infrastructure development. We also recommend steps that can be taken to limit the risks of potential cost increases associated with this growth for existing customers.

Northern Virginia currently has the highest concentration of data centers in the world and remains the fastest-growing market; by some estimates, about 70 percent of global internet traffic flows through the region. Virginia also has ambitious clean energy goals enshrined in the Virginia Clean Economy Act (VCEA), which requires the state’s investor-owned utilities, Dominion Energy and Appalachian Power, to achieve 100% clean electricity by 2045 and 2050 respectively. This is parallel to the ambitious clean energy goals that many data center and technology companies themselves hold.

To examine the transformation of Virginia’s electric sector under rising data center load growth, E3 conducted a detailed PJM-wide assessment of multiple load growth scenarios using our in-house reliability and capacity expansion models, RECAP and RESOLVE, as well as a cost of service study to examine the impacts on residential customers under different cost allocation methods.

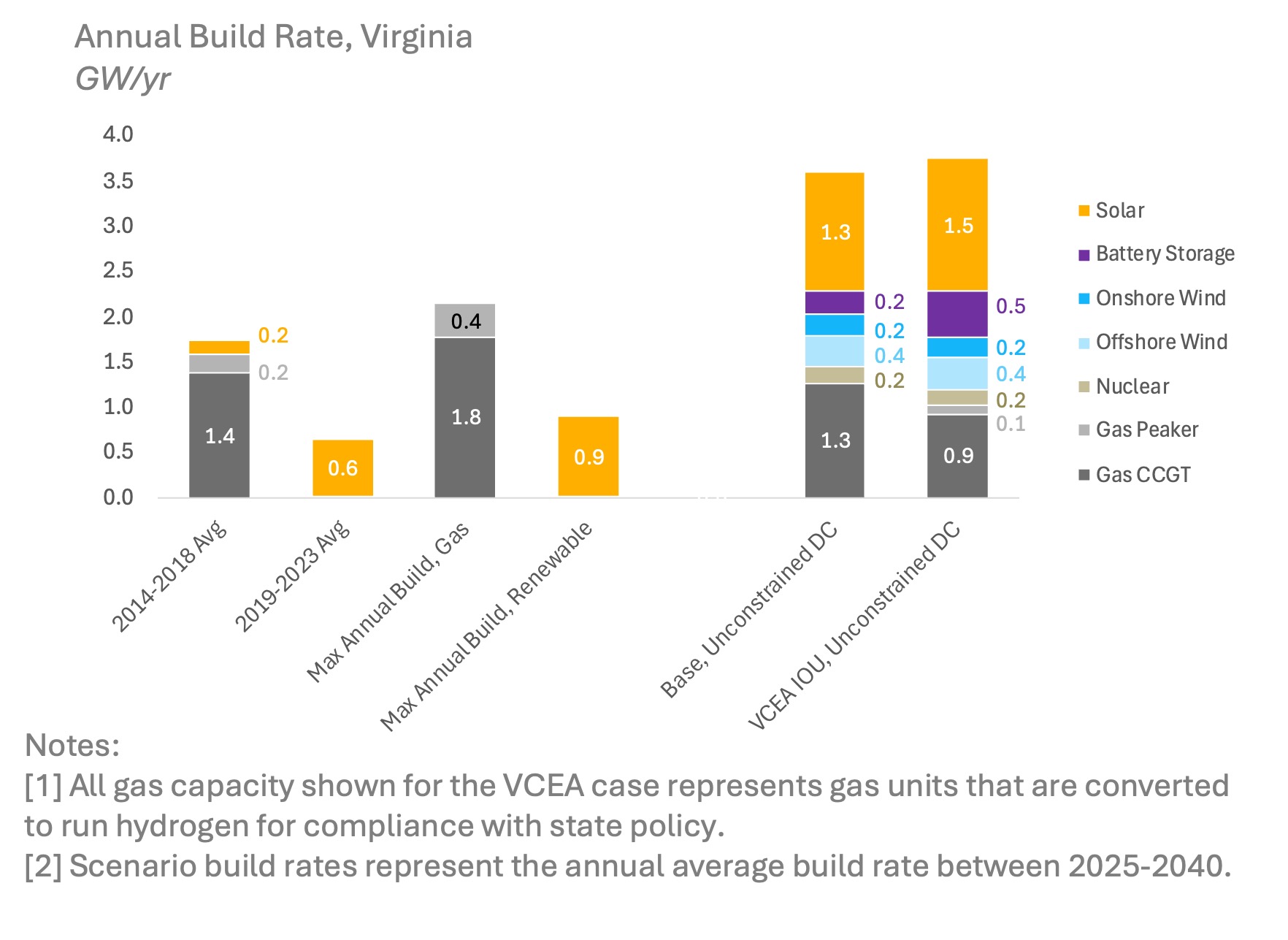

E3 collaborated with the University of Virginia’s Weldon Cooper Center (WCC), which developed independent projections for data center growth in the state. If current trends continue without any constraints on growth, WCC projected that electricity demand in the state would more than triple relative to today’s levels, which would place significant pressure on system planners’ ability to build sufficient generation, transmission, and distribution infrastructure to maintain a reliable system. Our analysis finds that achieving Virginia’s clean energy goals set forth in the VCEA while also serving “unconstrained” data center growth would require unprecedented investments to accelerate the deployment of both existing and emerging clean energy technologies. Virginia and the broader region would need to rapidly expand the build-out of existing clean energy resources like solar and offshore wind, with sustained in-state solar additions much greater than historical highs (1.5 GW/yr compared to a single-year high of 0.9 GW/yr). In parallel to this expansion of existing clean energy resources, the state will also likely be required to make transformative investments in emerging technologies such as new nuclear capacity and hydrogen-ready combustion turbines, as well as a major expansion of interzonal transmission capacity and an increase in the state’s reliance on purchases from the PJM wholesale electricity market.

Even in a scenario without the VCEA, data center driven load growth would require sustaining a very high pace of new capacity additions through 2040, including a significant expansion of the state’s reliance on natural gas. The pace of infrastructure development would far exceed what has occurred in Virginia in recent history (3.6 GW/yr over the next 15 years, compared to a historical single-year high of 2.2 GW).

Our study concludes that the pace at which utilities, developers, and state regulators (in coordination with the broader PJM market) can accelerate their processes for siting, permitting, and building new infrastructure will very likely act as a constraint on data center growth in the near to medium term. However, grid interconnection policies protect electric system reliability by delaying new load from connecting until the infrastructure to serve it reliably is in place. These policies protect the reliability of the system for existing customers, but will constrain data center load growth to the rate of infrastructure expansion.

The significant, sustained investments in new infrastructure to meet rapid data center growth also present affordability risks for the state’s existing electric customers if the projected electric load fails to materialize at the levels currently forecast. Because current electricity rates appropriately apportion costs to the customer classes responsible for incurring those costs, historic “cost-shift” from data center load to date have been minimal. Going forward, however, the pace and scale of infrastructure development built as well as secondary impacts such as increasing tightness in energy and capacity markets is likely to lead to upward pressure on rates for all ratepayers in the near to medium term. Our report identifies steps the state and its utilities can take to further reduce the risk of future cost shifts as data center growth continues to accelerate. Such steps may include improving the frequency of updates for cost allocation factors; improving forecasting of data center demand through features like a waitlist for service that can derisk load attrition; and implementation of long-term service commitments that may include more significant minimum charges, among other recommendations.

Find the full report, including a detailed examination of the impacts of data centers on system reliability, generation and transmission investments, and resulting impacts on residential ratepayers, here.

Download the report.

This report was prepared by Kush Patel, Kevin Steinberger, Andrew DeBenedictis, Manfei Wu, Jonathan Blair, Paul Picciano, Pedro de Vasconcellos Oporto, Brendan Mahoney, Andrew Solfest, Riti Bhandarkar, and Aneri Shah.

E3 would like to thank JLARC and WCC for their timely input, data, and perspectives throughout the engagement. We would also like to thank the experts interviewed for this work, including representatives from load-serving entities and several data center companies for providing their perspectives and insights on data center growth, operations, and cost of service studies. The analysis presented in this report is solely reflective of E3’s views and perspectives in the context of the scope of work; all conclusions and takeaways are our own.