E3 is excited to announce the public release of its first annual resource cost forecast package, created using our in-house Recost model.

This release contains two products:

- Public Outlook: available for free, this report summarizes E3’s forecasts and perspectives on the resources critical to the energy transition.

- Recost Model and Assumption Details: available for purchase, E3 is now offering the Recost model used for our market price forecasts and additional details behind our assumptions and methodology. The model includes all inputs, assumptions, and calculations, and can be configured as needed by the client after purchase (for example, state-specific capital and operating cost adjustments may be selected that are not included in our Public Outlook).

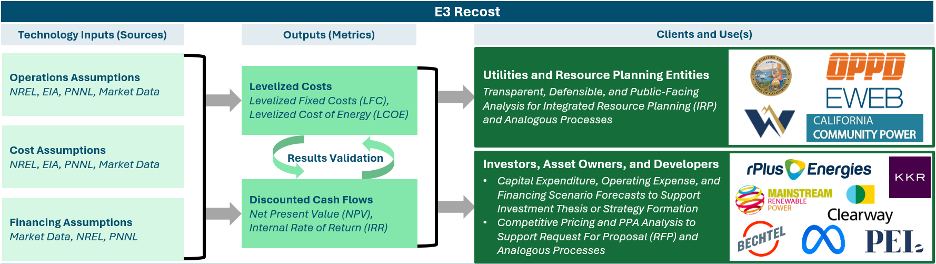

Recost is a discounted cash flow model that computes levelized cost metrics, such as the levelized fixed cost (LFC, $/kW-yr) and levelized cost of electricity (LCOE, $/MWh). E3 aggregates, synthesizes, and develops the set of technology- or project-specific assumptions for system performance and operations, upfront and ongoing costs, financing parameters, and state- or province-specific cost adjustments used in Recost. We also combine fixed cost calculations with resource-specific capacity contribution assumptions to develop a levelized cost of capacity (LCOC) metric, also known as gross cost of new entry (Gross CONE). Results from the Recost levelized cost calculation can be used in a wide array of electricity system planning contexts including capacity expansion modeling, market price forecasting, procurement strategy and bid evaluation, electrolytic fuel cost estimation, and others.

Since 2010, E3 has regularly created and released formal databases and calculations of levelized costs for its clients. Recost has been used across multiple public engagements, such as the Western Electric Coordinating Council’s transmission planning studies, the California Public Utility Commission’s Integrated Resource Planning Process, New York’s Scoping Plan, as well as integrating resource planning processes for individual utilities such as the Omaha Public Power District, Sacramento Municipal Utilities District, Nova Scotia Power, and others. In addition, E3 leverages Recost to create our market price forecasts across all U.S. markets, and to support confidential investor engagements.

Now, E3 is offering the full Recost model and detailed analysis with Q4 2024 assumptions and forecasts for purchase “off the shelf” on our website.

In the Q4 2024 release, E3 finds the following:

- Long Covid, meet the energy transition: Post-Covid shocks embedded in long-run costs

- Declines in the costs of resources key to the energy transition (onshore wind, utility-scale solar, and battery energy storage systems) were impeded, halted, or reversed between 2020–2023. With the cost spikes from recent years now fully embedded in our forecasts, the message is clear: cost levels have not returned to the pre-Covid expectations for 2025, and there are multiple strong headwinds facing any return to pre-Covid cost reduction paths.

- What’s in a name? The Inflation Reduction Act begins to shape post-inflation economics

- In E3’s view, the primary energy-sector impact of Inflation Reduction Act (IRA) is the pressure applied to reduce resource costs closer to pre-Covid trajectories. Looking ahead, IRA incentives are the most meaningful path to sustained national power sector decarbonization, and the certainty provided through 2032 is a boon to clean energy sector growth. Beyond 2032, development trajectories are more uncertain than before, as the sector enters the period during which the sunset provisions of the Act may be triggered.

- The new, complicated normal: complexity is now a feature, not a bug of the energy transition

- Reduced learning curve impacts for mature clean technologies and more rapid potential cost declines for emerging technologies will continue, but U.S. industrial policy now means that location matters more than ever before; it will be difficult, if not impossible, to discuss a “generic” project over the coming decade.

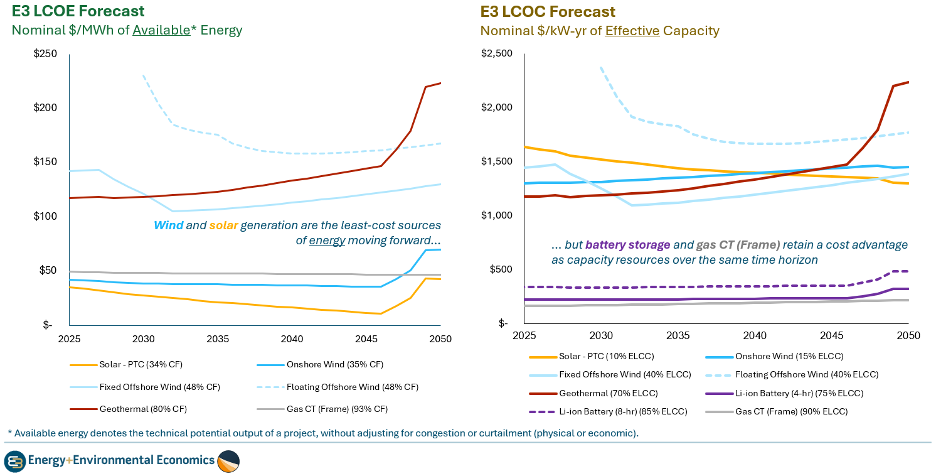

A summary of E3’s Recost outlook under different resource-specific assumptions is shown below. We find that solar and wind at good sites generally have lower LCOE than conventional natural gas generation when emissions aren’t priced. However, LCOE is not by itself a measure of a resource’s competitiveness because it doesn’t consider differences in the value of the energy produced at different times and locations. Lithium-ion batteries and gas CTs have the lowest LCOC, however, capacity accreditations may vary by market. Battery accreditations will likely decline over time as penetrations increase. CT accreditations may depend on firm fuel availability.

For more information on Recost and other E3 models, see here.

For the Q4 2024 Recost outlook, see here.

For more details on purchasing the full outlook analysis and E3’s Recost model, see here.